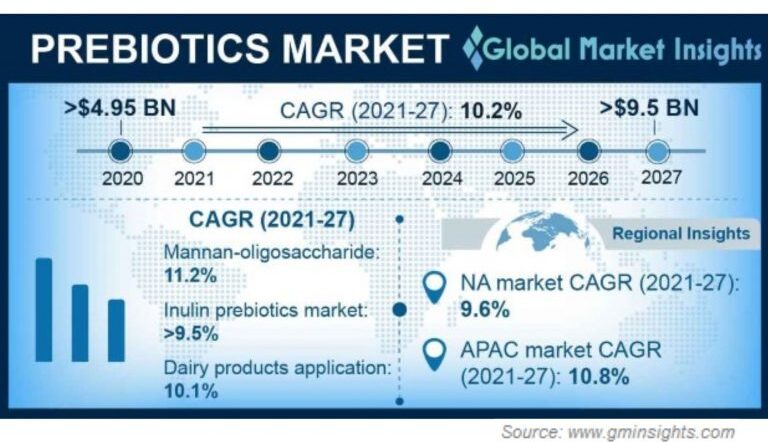

Current Market Trends

There’s no doubt about it, inulin is the leading prebiotic fiber in the industry, but scarce sources, tariffs, fuel costs, and hindered transit routes have driven the price up astronomically. Unfortunately, this trend is expected to continue well into 2027 (4). During the summer of 2021, the key producing regions of chicory root in Europe experienced unprecedented wet conditions—causing an increase of defects and diseases in the chicory roots (1). As a result, prices soared while availability declined. Food developers were forced to either comply with the inflated prices, reduce their product portfolio, or seek alternative fiber sources and reformulate.

Because of acreage expansions in France, Belgium, Poland, and Germany, European chicory harvest yields were expected to increase 10 to 15 percent in 2022 (1). However, the quality of the harvest won’t be known until October—the harvesting process can take two months to complete, if the weather conditions are favorable (2). Harvest yields aren’t the only factor to consider though. Even if the chicory supply becomes available, it may not be available for food and beverage manufacturers—or it may not be available in the quantity needed for standard production. Market research has shown that the greatest call for inulin has been coming from the pharmaceutical sector (3). As the health benefits of inulin became more well-known, so did its applications. Despite supply chain complications, consumer demand for foods rich in prebiotic dietary fibers has continued to escalate.

Limited allocation and sparse sourcing has caused the cost of chicory root inulin to skyrocket. Many food and beverage companies have been compelled to rollout price increases just to keep up. On the subject of operation costs, Ingredion stated: “2021 was a year for unprecedented cost increases. In 2022, we continue to experience extraordinary market conditions which have been further impacted by the unfolding events in Eastern Europe, and markets remain highly volatile. These unforeseen increases have had a dramatic impact on many cost drivers so far…”. This statement was followed by a product list with marked up prices. So, how do we as suppliers of natural food ingredients move forward in the face of these uncertain market trends?

Looking to the Future

At Icon Foods, we’ve shifted gears. Our Prebiotica FOS and FibRefine Soluble Tapioca Fiber product lines have grown in popularity as plug-in replacements for inulin. Fructooligosaccharides (FOS) and inulin have a great deal in common. They’re both considered dietary fibers by the FDA and pass through your small intestine undigested. They’re both excellent sugar replacers, fat replacers, texturizers, and sources of high fiber bulk. They both improve gut health by turbocharging your microbiome. In fact, when you see and taste them side by side, they are virtually indistinguishable from each other—there is a very good reason for that: oligofructose is a subset of inulin! Fructooligosaccharide is referred to as inulin if the average fructan chain length is 6 or above. When the average chain length is between 3 and 5, it is referred to as fructooligosaccharide or oligofructose.

Inulin

All forms of inulin are still very pricey; particularly chicory root. There just isn’t enough chicory and the war in Ukraine has not helped with that matter. Jerusalem artichoke and agave inulin are certainly stable—if you’re willing to pay a higher price. We have moved many of our customers to FOS. While FOS may not have the gelling properties of chicory, Jerusalem artichoke, or agave—due to its chain length—FOS does hold up well in most processes and is a fantastic prebiotic fiber. Mixing FOS with soluble tapioca fiber will give your formula excellent gelling and it stabilizes any potential gastrointestinal effects that may occur from too much dietary fiber.

FOS

Fructooligosaccharides (FOS) are short-chain polymers comprised of D-fructose and D-glucose, which are not metabolized by the body like simple sugars, and are, therefore, considered non-digestible oligosaccharides. This cost-effective alternative can save manufactures time and money—alleviating their need to source costly inulin. One of the best value propositions of FOS is labeling. It shows up well on the NFP but, also gives you flexibility on the ingredient statement. When listed as a prebiotic fiber or FOS, the ingredient statement won’t need to be altered should you choose to transition back to inulin when the sources are easier to access.

Soluble Tapioca Fiber

Soluble tapioca fiber is the gold standard for fiber from an Icon Foods perspective. The price will not be driven up by the corn shortages that are currently effecting the market. It is not manufactured in China—thus not subject to the 25% tariff. Functionally, RS4 resistant dextrose or resistant starches add fiber and work well in low-carb, keto applications where fiber is needed to contribute to mouthfeel.

Sources

- Aditya. “Global Inulin Market Scenario for 2022.” Beroe Inc., Beroe Inc, 12 Aug. 2022, https://www.beroeinc.com/article/global-inulin-market-scenario-for-2022/.

- Folnović, Tanja. “Chicory Harvest.” AGRIVI, AGRIVI, 6 June 2022, https://www.agrivi.com/blog/chicory-harvest/#:~:text=Chicory%20is%20typically%20farmed%20in%20a%20biennial%20cycle%2C,yellowing%20and%20the%20inner%20leaves%20are%20still%20green.

- “Inulin Market.” Transparency Market Research: Food and Beverages, Transparency Market Research, July 2021, https://www.transparencymarketresearch.com/inulin-market.html.

- “Prebiotics Market Share Report 2021-2027: Global Statistics.” Global Market Insights Inc., Global Market Insights Inc., Apr. 2021, https://www.gminsights.com/industry-analysis/prebiotics-market.