Market Intelligence Report: Entering Q3 2024

By Thom King – Chief Innovations Officer, Icon Foods

Here we are emerging out of the 2nd quarter. It feels like Q1 was just yesterday. First let’s talk about the sticky situation within the sugar industry. If you work with sugar, in the words of Jay Z, “I feel bad for you son.” The price of sugar has risen faster than a well-baked soufflé. Unforeseen weather patterns causing crop failures and shortages, combined with the temporary shutdown of the largest port for imports (Baltimore), has had a significant impact. And while there have been some pullbacks in price, it doesn’t look like the supply chain will course correct any time soon. Albeit, from time to time there is a dip in price that gives commodity traders’ hearts a little pitter-patter.

Even the FDA and USDA have piled on “enemy number one.” With front of pack callouts for added sugars and the school lunch program’s new guidelines on the horizon, this has truly been a bad time for sugar.

The cocoa supply chain has been as convoluted as a box of assorted chocolates. Cocoa prices have tripled over the past 12 months, following ongoing bean disease in West Africa. Cocoa farmers there have been hit by several plant diseases that are ruining crops on a vast scale and pushing up the global price of cacao.

Right now, there is no relief in sight. In talks with some folks deep in the industry, there seems to be a consensus that cocoa will be used primarily for confections, while inclusions, covertures and coatings will start migrating over to palm kernel oil and fibers to stretch out cocoa usage. I have tried some of this in our lab and it’s actually quite good and even friendly on the ingredient declaration.

As my Irish grandfather used to say, “where you find 4 priests, you are likely to find a fifth (of whisky),” and to that point—where there are challenges, you may still find opportunities. Now might be a great time to lean into clean label sugar reduction and reformulate some of your dusty old formulas. Icon Food Science is here to help.

Overall Economy and Food Prices

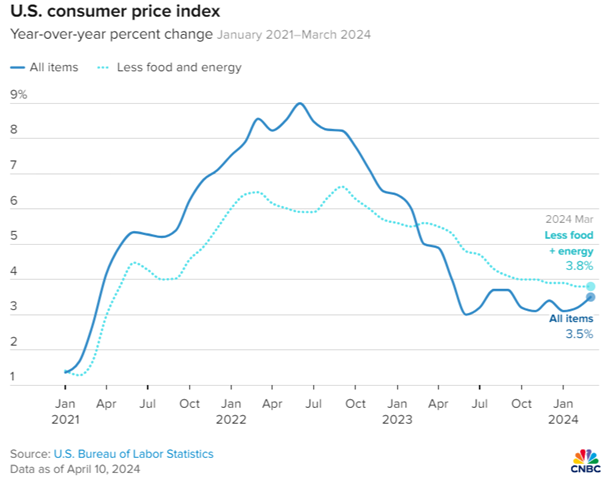

“It’s the economy, stupid,” said James Carville in 1992. The phrase has never been more appropriate. The U.S. economy experienced slower growth in the first quarter than initially estimated due to downward revisions in consumer spending and a slight decrease in a key measure of inflation. This trend may lead the Federal Reserve to consider cutting interest rates at least once before the end of the year.

The economy is cooling, and folks are buying less stuff—including snack foods. Most CPGs in the snack food category have seen declines in demand. Mondelez International confirmed this in a recent presentation, stating they saw snack volume decline amid “mixed” consumer confidence (8).

The Shift in Consumer Eating Trends – The Opportunity

In a recent Bloomberg article entitled, “Food Companies Want a Piece of the Ozempic Pie, Too,” author Amanda Mull wrote, “Yes, GLP-1 drugs, as medications in this class are often called, do tend to make their users less hungry and less impulsive, and they can also make greasy or rich foods unpalatable or difficult to digest for some.

What they don’t do, though, is exempt anyone from eating…For food brands, any group with a particular set of unfulfilled desires is a market waiting to be addressed, and in Reddit and Facebook communities for people taking these drugs, those newly prescribed ask the same few questions constantly. Chiefly among them: What do you guys on these meds eat?” (1). This paragraph pretty much sums up where the opportunity lies.

Food and beverages tailored towards the GLP-1 diet will be a massive trend over the year as more and more folks jump on the GLP-1 (Ozempic) train. If your brand struggled in 2023, 2024 could be your year if you formulate nutrient dense foods that are easy on the GI.

Corn

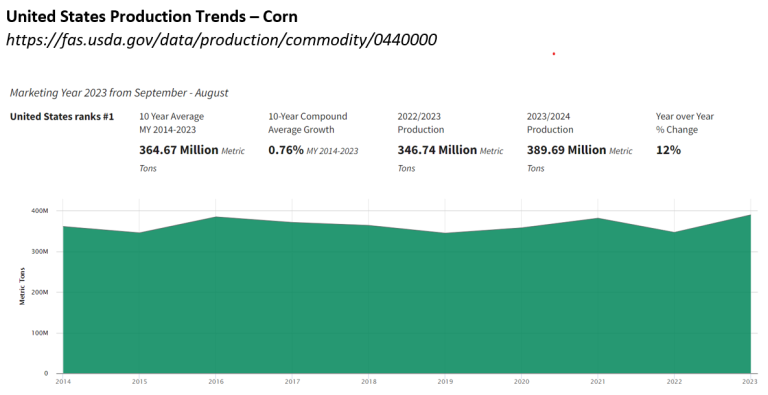

The prevailing question is, “how does corn affect me?” Corn is the richest source of glucose; glucose is the most efficient substrate for polyols like erythritol, rare sweeteners like allulose, and everything in between—acidulants, gluconates, and the list goes on. If there is an abundance of corn and the price is way down, it makes sense that corn derivatives will follow suit. The US set yet another corn crop record, surpassing last November’s 174.9 bu/acre with over 177.3 bu/acre (7). Ladies and gentlemen, we are flushed with corn. This will likely exert downward pressure on corn derivative commodity prices, and if the power brokers allow it, could lead to consumer prices going down too.

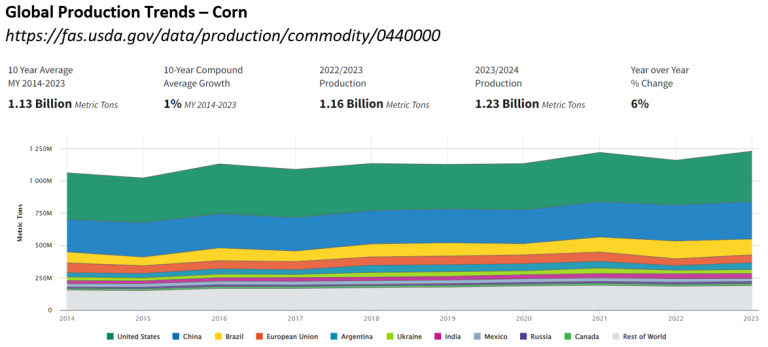

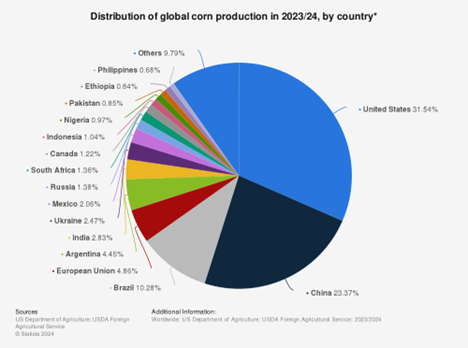

While the US is going gangbusters with corn crops, the global outlook is not so sunny. The International Grains Council (IGC) has revised its 2024 global corn production forecast downward by 6 million metric tons (MMT) from last month, bringing the total to 1.220 billion metric tons. This adjustment reflects significant reductions in Argentina and sub-Saharan Africa. Consequently, the global corn crop is now expected to decline by 5 MMT (0.4%) compared to last year, contrary to the previous forecast that predicted an increase (6).

The result of this decreased yield could translate into upward pressure on corn derivatives manufactured outside of the US, such as China. This is where most erythritol and allulose are made. I will explore this further down in each of the commodities.

In case you were curious, the graph below illustrates which countries are the biggest exporters of the golden kernels.

Logistics

After a two-month period that should have lasted over a year, federal agencies announced this week that full access for commercial maritime transit through the Port of Baltimore has been restored. This follows the removal of 50,000 tons of debris from the March 26 collapse of the Key Bridge (9). Crazy, right?

The fully operational channel will allow two-way traffic and the ending of the additional safety requirements that were required because of temporary reduced channel width. Can I get a hell yes?

However, don’t be lulled into complacency. A shift is coming, and if you start planning now, you can get ahead of the trends and mitigate the impacts on your business. Domestic and global factors are expected to drive capacity correction and rebalance freight rates in just six months’ time. The bridge collapse has accelerated that timetable (10).

Rising Ocean Container Volumes

Pre-COVID volume patterns are returning. FreightWaves reported “clear growth” for maritime imports in comparison with pre-pandemic years — and the early evidence is already materializing at our West Coast ports (10).

According to Allison Dane Camden, deputy assistant secretary for multimodal freight infrastructure and policy at the U.S. Department of Transportation, “We’re starting to see a little bit [of an uptick]” in containers going to the West Coast, based on data from DOT’s Freight Logistics Optimization Works initiative. We are watching for a shift back, now that Baltimore is open (10) .

Panama Canal and Suez disruptions

The Panama Canal Authority has scheduled new measures designed to increase capacity and alleviate some of the restrictions that affected transit in the past year. The latest steps—in addition to increasing capacity—also address the concerns of larger containerships and LNG carriers (3).

Starting in July, they will add an additional slot to each set of locks. The Neopanamax Locks will have an extra daily slot, bringing the total to nine daily transits as of July 11. The Panamax Locks will add a slot on July 22, increasing its daily transits to 25 (3).

Total daily transits will increase to 34 as of late July, moving toward the goal of 36 to 39 daily transits by 2025. At the peak of the water crisis, the Panama Canal Authority had lowered the transits to a total of 22. They had mapped a further step to 18 daily transits, but were never required to implement those restrictions (3).

Especially significant for the larger vessels, they are increasing the maximum draft by one foot to 46 feet as of June 15. The canal, which has at peak times been as high as a 50-foot draft, had been operating at 44 feet, although it returned to 45 feet at the end of May. In 2023, the Panama Canal Authority mapped a strategy that called for lowering the level first to 43.5 feet and possibly as low as 39 feet. Even at the 44-foot level, some vessels were being forced to divert, or transit with partial loads. Some containerships were transshipping boxes across the Isthmus by train to meet the draft restrictions (3). More good news.

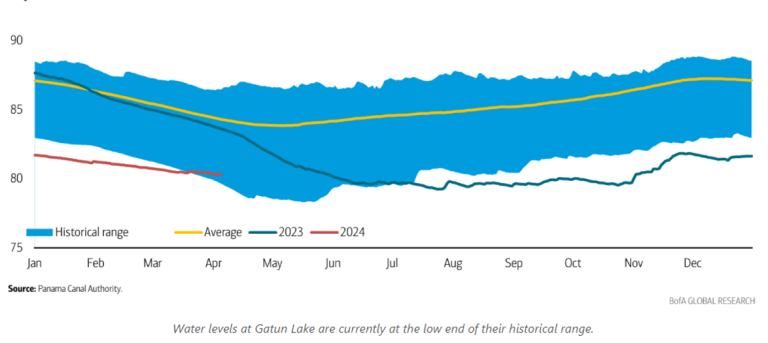

Water Levels at Gatun Lake

A recent downpour was gladly received by the man-made Gatun Lake from which the canal gets its supply of water. Traffic has seen an uptick in the past few days: Per data from Clarksons, transits are currently at 60% of where they were in 2022, a year in which conditions were more or less normal. Transits of product tankers and container ships have almost fully recovered, with both types trending near 90% of normal activity. We are optimistic that canal operations will return to normal by 2025 (4).

Likewise, conflict on the Red Sea is still creating delays. There are still premiums on containers prices as container ships wait for naval escorts to the Suez Canal or reroute around the Cape of Good Hope. This adds about 9 days to transit.

Summer Fuel Price Surge

The summer driving season is here and, with it, historically the return of higher fuel prices (10).

The impact is twofold: First, these costs will be passed on to shippers in the spot freight market. Second, carriers locked into unsustainable, rock-bottom contract rates and without sufficient cash reserves will be forced out of the market when that cash dries up— which in all likelihood will tighten capacity and further drive up costs (10).

These converging conditions will likely mean minor shipping delays and upward pricing pressure.

The tea leaves say we’ll likely be looking at upward pressure on the freight market and tightening capacity by fall and winter of 2024. While we may be three to four months out from a market shift, the time to start planning for it is now. The key to happiness and a low stress life? Planning ahead.

Tariffs

I have learned to despise the word tariff. Like me, I am sure there are plenty of you who have been waiting on pins and needles for the current administration to reverse those Trump era tariffs. It’s fair to say we have been disappointed, but isn’t that the case with expectations? We all need to grow up already. One might wonder, why do we still keep tariffs? They just drive-up costs for manufacturers, that then trickle down to the consumer and constitute the cycle of inflation. Let me explain where those tariffs go.

The tariff goes to the treasury department, and they use it for whatever they want. Mainly, it is a rather surreptitious way to raise taxes on the middle class without really raising taxes. Right now, here is a lot of bluster from the current administration—they are considering an increase in the current tariff. Trump has suggested a 60% increase. We are keeping a keen eye on this because once a tariff is in place, it is very very hard to turn back. Again, plan ahead. Get positioned in your raw materials.

Erythritol

Erythritol is still at historic lows. It may stay this way for the next few months, but the Magic Eightball says that a market contraction will put upward pressure on pricing.

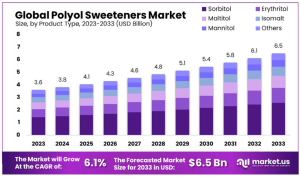

From a food scientist perspective who does a lot of formulating, I am often asked, “is anyone actually formulating with erythritol anymore?” The answer to that question is an unequivocable yes. There is still a lot of formulating going on with erythritol. Whole Foods, Health Canada and the EU don’t allow allulose, leaving few viable options. But, clearly based on the graph below, erythritol is still enjoying consistent year over year growth, indicating continued consumer demand. Sure, erythritol’s perception can be mixed, but it is far from the sullied reputation of sugar and aspartame.

Projected figures anticipate growth from USD 4.03 billion in 2023 to USD 6.2 billion by 2030. This reflects a compound annual growth rate (CAGR) of 6.1% during the forecast period spanning 2023 to 2033 (5). A better return than a certificate of deposit.

Though the price is nice and low, as I mentioned, we will start to see upward pressure. Likely around August. Secure your position.

As we see the global corn market starting to contract, the remaining surplus material will dry up, creating upward movement on price and tightening of supply. August 2024 there will be an upward turn.

Call your Icon Foods representative and help us help you get your erythritol needs locked down through July of 2025.

Allulose

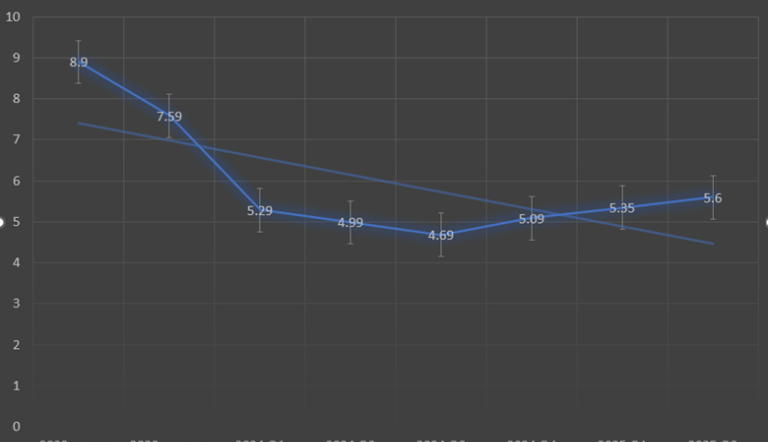

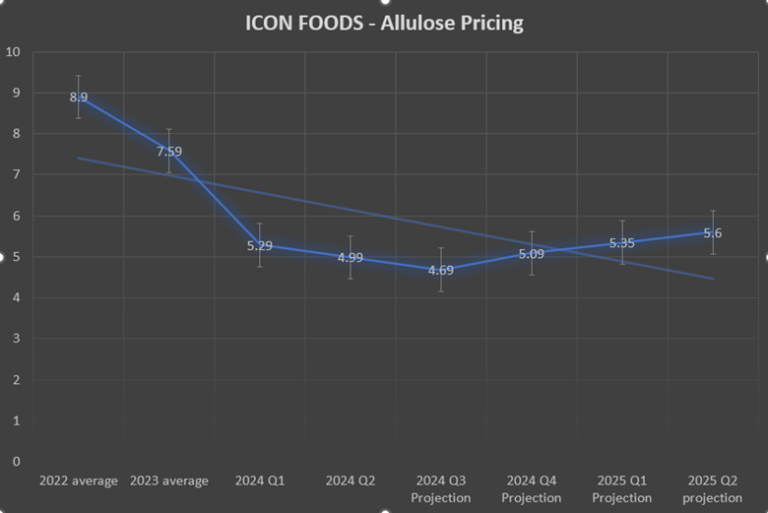

There were several new high-quality producers of crystalline allulose that started scaling in 2023 resulting in more product in the market in early 2024. As you can see in the graph below, this has created downward pressure on pricing. Prices went down about 3-5% over the last quarter. While the price of allulose syrup remains very stable, crystalline allulose has trailed behind. Supply has increased by about 10 MMT, which is driving pricing down as more of this material enters the market. New technologies will have had a downward impact on allulose pricing, with more to come in 2025.

The only thing stopping allulose from being the be-all and end-all in the sweetener arsenal is approval with Health Canada, the EU and Whole Foods. I am not one to spread rumors, but based on the scuttlebutt in the commodity sewing circle, there is an expectation that first quarter of 2025 will bare good news.

I honestly thought this was BS when I stumbled across it (I can not name the source), but there has been a substantial spike in demand. Many of the main manufacturers and suppliers are fully allocated through the remainder of the year. If a positive decision is made and allulose is approved as a food ingredient in the EU, the remaining outliers will fall in line. This would increase demand at least six-fold, and with increased pressure on the supply chain, prices will rise rapidly.

Like a broken record, I am going to repeat myself. Get ahead of this. Position yourself through June of 2025. You won’t be sorry.

Below is the trend line for allulose.

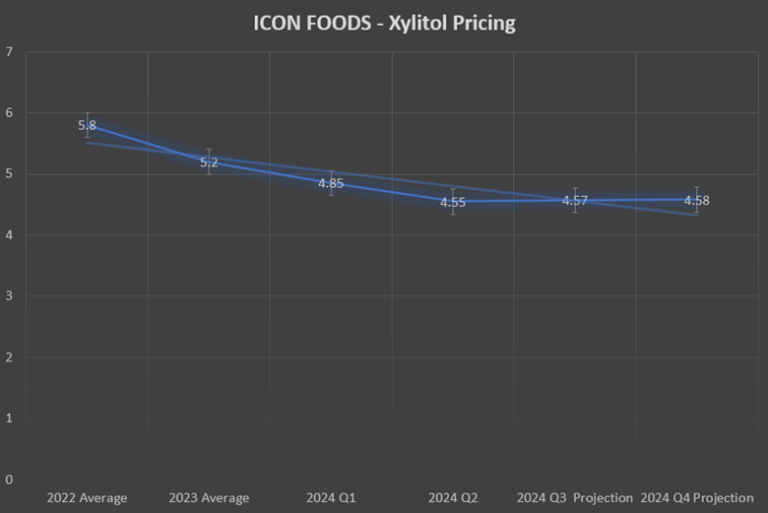

Xylitol

The global xylitol market size was valued at USD 701.5 million in 2023 and is poised to grow at a significant CAGR of 4.3% during the forecast period 2024–30.

Xylitol prices have been rising over the past few months. This is likely from some brands moving away from erythritol. If xylitol and erythritol are pretty close to the same manufacturing process, then why is it that xylitol is so much more expensive? It comes down to water and power—a lot of water and a lot of power is required to get the d-xylose out of the corn cobs and corn by products. China also has a heavy tax on water usage and expensive electricity. Most xylitol is derived from corn cobs that do not birch as some people have been led to believe. Since xylitol is a corn derived ingredient, its cost may rise with the price of corn and when availability wains—which is likely to happen in late August 2024. This would be an ingredient worthy of hedging right now since costs could rise on a tightening global corn market.

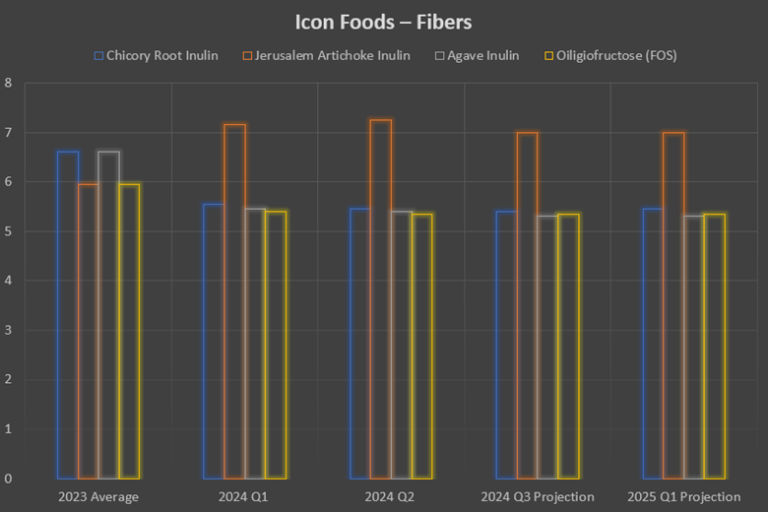

Inulin

The chicory root inulin supply chain is quite solid; pricing is stable and even down some since a lot of manufacturers moved away from chicory root inulin to FOS when the price was sky high and supply chains were non-existent. Agave inulin is certainly stable, but somewhat pricey. It appears the abundance of chicory root inulin is putting downward pressure on the other inulin type fibers, except for Jerusalem artichoke, which presents a rather poor value as a medium chain fructooligiosaccharide. Jerusalem artichoke shares a similar degree of polymerization with chicory root and agave inulin. There is no compelling reason to use it as a main fiber source.

While FOS may not have the jelling properties of chicory, Jerusalem artichoke, or agave—mostly because of chain length—FOS still holds up well in most processes, dissolves quickly with little turbidity, and is a fantastic prebiotic fiber. Stacking FOS with another inulin of different chain length along with soluble tapioca fiber will allow for more fiber in your formula, giving you excellent gelling and stabilizing whatever potential gastro-intestinal effects that may occur from too much dietary fiber. You will see this fiber stacking in many of the up and coming better-for-you beverages.

FOS

Most of what I needed to say about FOS is in the inulin paragraph. Icon Foods is well stocked and well positioned with FOS. The price is very good and can save manufacturers money compared to inulin. One of the best value propositions of FOS is labeling. It shows up well on the NFP, but also gives you flexibility on the ingredient statement. When called out as prebiotic fiber or even FOS, you can switch between inulin or FOS without having to change all your packaging. Food for thought when considering your fibers.

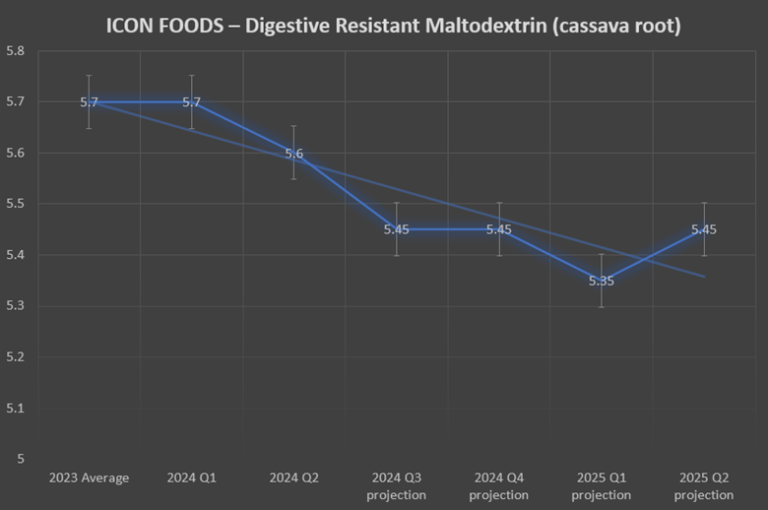

Soluble Tapioca Fiber

Soluble tapioca fiber remains the gold standard for fiber from an Icon Foods prospective. The price will not be driven up by the corn market. Icon Foods’ FibRefine is not manufactured in China, thus not subject to the 25% tariff. Functionally, it’s an RS4 resistant dextrose or resistant starch that adds fiber and works well in keto and low-carb products, and in applications where fiber and exceptional gelling properties are needed to contribute to mouthfeel. Icon Foods is very well positioned in soluble tapioca fiber. The price is much lower than soluble corn fiber and you won’t have “corn” on your ingredient dec. As I mentioned, this is the gold standard and many functional beverage companies and food manufacturers are migrating over the soluble tapioca fiber to get the grain free claim. I would look for supply to contract starting Q3 of this year as upward pressure on cost may start in Q4 2024 and continue into 2025. Global warming will likely trigger extremes in weather in Southeast Asia. Cassava Root, which tapioca is derived from, is susceptible to extremes. If crops crash, shortages can happen very quickly and so can price escalations. Lock in for price stability.

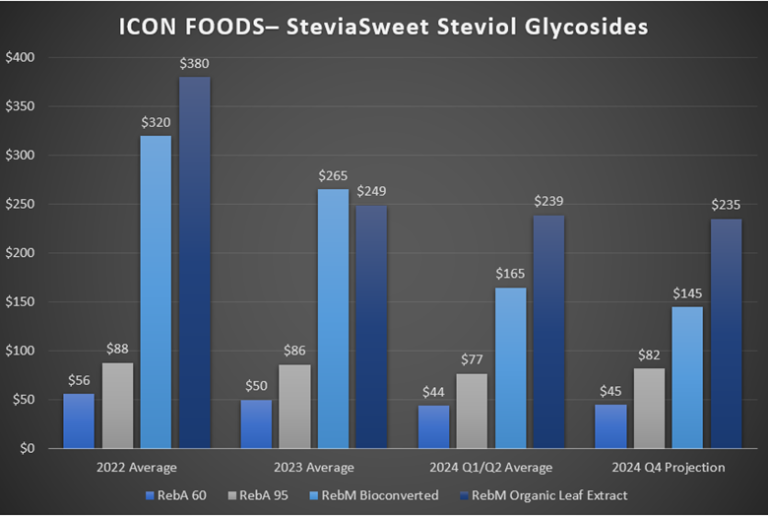

Stevia

China produces over 80% of stevia extract distributed around the world—having a finger on the pulse of this sweet commodity can really help with predictive analysis when it comes to pricing.

Last September’s harvest was glorious for stevia leaf and leaf used to convert to higher grade extracts. Supplies have contracted and prices have started to slowly climb.

2024 planting area of stevia this year increased by 20% – 30%. More planting area means more plants and higher yields. We could see prices come down in early 2025. Stand by.

As a note, nearly all stevia is propagated from clippings and grown in massive green houses that stretch for hundreds of miles. The ratio of seedlings to seed crops is 95% verse 5%. Clippings enable the plant to leverage specific glycosides, like Reb M for instance. This has contributed to a significant drop in price in comparison to when this specific glycoside was first isolated and commercialized. It will continue to increase in efficiency and make Reb M a more affordable option.

The stevia harvest occurs in September, the bounty of extract will likely start showing up in early November 2025. Prices for leaf extract will see upward pressure now through Q3 as last year’s stock gets depleted. Lock your position in now to get over the price jump.

If your need is organic leaf extract, the prudent buyer would lock their positions in through June 2025. While prices may rise over the next few months, never fear—like all things in this world, it will be temporary. Look for pullback in the late Q4 2024 or early Q1 of 2025.

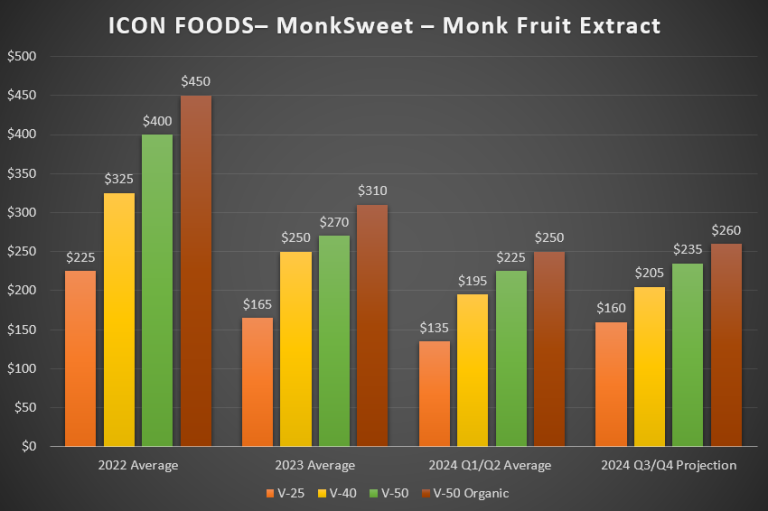

Monk Fruit

After a significant spike in price in 2022 followed by a slight stabilization in 2023, early 2024 experienced further discounts as manufacturers depleted older 2023 material. Right now is the time to lock in your monk fruit. Stretch your stock out as far as you can—even as far as June 2025. Over the next 2-3 months monk fruit prices will rise 4-6% and possibly a little more. Late July buyers will start to see the typical upward pressure on pricing because of depleted stock. There could be a jump of 15-20% in Q4. While 2023 brought a record harvest that triggered significant price drops in Q1 finished goods, any leftover material is now edging up. At best you have until July to take advantage of the remaining stock. I would stock up.

Summary

Sugar and cocoa prices are way up, but consumer demand is falling. Consumers are becoming more savvy about what they put in their mouths. Consumer adoption of GLP-1 agonists has caused a shift in ultra-processed food sales. Walmart’s pull back on processed food revenue nearly matches the market adoption of GLP-1’s.

Consumers are changing their eating habits due to these weight loss medications like Ozempic. As a result, several large CPG brands are reevaluating their portfolio in response to the changing needs of shoppers. Nestle launched a new brand a couple of weeks ago. Abbott Laboratories launched a new brand of protein shake in January that targets adults who are attempting to lose weight and maintain muscle mass.

It’s like nothing I’ve ever seen—the market is wide open and rife with opportunity for those courageous enough to jump in. If you thought keto was big, GLP-1 will dwarf that trend. Icon Foods is here to help with our sweeteners, sweetening systems, sweetness modulators, fibers and inclusions all designed to make deep clean cuts to added sugars and make your NFP shine. Icon spells innovation.

From my vantage point, consumer spending is on the rise. The economy hasn’t been this vibrant in a decade, jobs are plentiful, and there is a stir in innovations. Most of these innovations are trying to get ahead of consumer demand and trends. This begs the question, where do you stand?

Thank all of you for your kind comments regarding my last market intelligence report. That means a lot, but what would mean even more is if you told me what I can do better and how Icon Foods can be a resource for you.

Thank you for your continued support.

Thom

Sources

- Mull, Amanda. “Food Companies Want a Piece of the Ozempic Pie, Too.” Bloomberg.Com, Bloomberg, 28 May 2024, www.bloomberg.com/news/newsletters/2024-05-28/nestle-s-vital-pursuits-is-just-the-first-ozempic-wegovy-marketed-food.

- Murray, Brendan. Bloomberg, Bloomberg, 25 June 2024, www.bloomberg.com/news/newsletters/2024-06-25/supply-chain-latest-global-trade-disruptions-and-shipping?cmpid=BBD062524_TRADE&utm_medium=email&utm_source=newsletter&utm_term=240625&utm_campaign=trade.

- “Panama Canal Continues to Restore Capacity after Drought.” The Maritime Executive, 11 June 2024, maritime-executive.com/article/panama-canal-continues-to-restore-capacity-after-drought#:~:text=Especially%20significant%20for%20the%20larger,at%20the%20end%20of%20May.

- “Panama Canal’s Future Is Dark and Stormy, Much to Shippers’ Relief.” Yahoo! Finance, Yahoo!, 15 Apr. 2024, finance.yahoo.com/news/panama-canal-future-dark-stormy-112700336.html.

- “Polyol Market Size, Share: Cagr of 7.1%.” Market.Us, 31 May 2024, market.us/report/polyol-market/.

- Pro Farmer Editors. “IGC Cuts Global Corn, Wheat Production Forecasts.” AgWeb, 23 May 2024, www.agweb.com/markets/pro-farmer-analysis/igc-cuts-global-corn-wheat-production-forecasts#:~:text=The%20International%20Grains%20Council%20(IGC,previous%20outlook%20for%20an%20increase.

- “Production – Corn.” Corn | USDA Foreign Agricultural Service, fas.usda.gov/data/production/commodity/0440000. Accessed 2 July 2024.

- Pymnts. “Mondelez Sees Us Snack Volume Decline amid ‘mixed’ Consumer Confidence.” PYMNTS.Com, 1 May 2024, www.pymnts.com/earnings/2024/mondelez-sees-us-snack-volume-decline-amid-mixed-consumer-confidence/.

- Shepardson, David. “Baltimore Port Key Channel Reopens Following Bridge Collapse | Reuters.” Reuters, 10 June 2024, www.reuters.com/world/us/access-fully-restored-key-channel-after-baltimore-bridge-debris-removed-2024-06-10/.

- “Tips for Navigating the Coming Capacity Correction.” FreightWaves, 11 Apr. 2024, www.freightwaves.com/news/tips-for-navigating-the-coming-capacity-correction.