Changing Imports

The days of gloom and doom are gone…right? I am not here to burst your bubble. In some ways, things are getting better. For some raw ingredients there is an excess of material. But for others, shortages remain. Currently, there are overstocks on dairy and most corn derivatives. So much so, that companies are dumping. Wait, what?!?! Did I just say dumping? If you are not familiar with the term, dumping occurs when a company exports a product at a price lower than it normally charges in its home market— “dumping” the product and flooding the market (2). While the World Trade Organization does not regulate companies engaged in dumping, it will occasionally punish them with a slap on the wrist for dumping their imports. The US government, on the other hand, does not take these matters as lightly. Tariffs can be sanctioned on the HS codes for countries violating anti-dumping agreements. What this says to me is get while the gettin’ is good. Cheap erythritol and allulose are not going to be here forever. By late Q1 we will all be singing a different tune.

Corn Imports

Remember imports in 2020? It seems like a lifetime ago. You might remember that back in 2020 China bought almost all the US’s corn stores to be used as animal feed—cementing their place as the US’s largest destination for corn and a leading corn importer globally. However, this may change. Let me explain. Until recently, China has sourced most of their corn from the US, with the remainder coming from Russia, Ukraine, and Brazil. Russia and Ukraine’s collective makes up about 17% of the world’s corn supply. Brazil has been the world’s third largest global corn producer for decades and the second largest exporter of corn for 2 years. In 2022, Brazil suffered an extreme drought that should’ve severely damaged their crop, but with the help of rich Russian fertilizer, they were able to export a very solid corn crop (8). China’s recent love of Brazilian corn presents a threat to U.S. dominance. Recently, China added more Brazilian corn traders to its list of approved imports—a sign that trade could begin imminently. Here’s something else to keep an eye on, U.S. purchases from China through mid-October were down 70% from last year. Whoa!

Another point of interest—Mexico imports 90% of their corn from the US. Recently, they proposed a ban on GMO corn which would comprise 90% of the US corn crop. Argentina is planting its 2023 harvest now and is poised to fill the gap left by Mexico’s ban should they instate it (4). The drama!

What it Means

Global total grains production, consumption, ending stocks, and trade are projected to decline in the marketing year 2022-23, according to the latest International Grains Council (IGC) Grain Market Report (6).

The report stated world total grains (wheat and coarse grains) output is expected to contract by 33 million tons in 2022-23, to 2.255 billion tons (down 1%), with smaller maize (down 53 million) and sorghum (down 1 million) crops more than outstripping increases for wheat (up 10 million), barley (up 6 million), oats (up 2 million), and other coarse grains (up 3 million).

Could the US really get shut out of the global corn market? We will see. This all translates to more corn stateside. And who controls that corn? Cargill, of course. But will Cargill be able to compete with Chinese imports of corn products? If they appeal to the federal government to put an anti-dumping tariff on the HS codes relating to corn derived products—which is just about everything from citric acid, polyols, citrates, and all things in between—then they might have a chance.

Here’s the thing though, the 2023 corn strips don’t reflect any of this. Futures strips are the buying or selling of futures contracts in sequential delivery months. They are typically used to lock in prices for specific time frames (7).

2023 Corn Strip — 6.6777 Up 0.0502

(12 months – January thru December)

MARCH ’23 — 7.0250

MAY ’23 — 7.0175

JULY ’23 — 6.9525

SEP ’23 — 6.4475

DEC ’23 — 6.2950

MARCH ’24 — 6.3625

In its preliminary baseline projections, as of October, the US Department of Agriculture forecast US farmers will plant more corn in 2023. Specifically, 92 million acres, up 3.4 million acres, or 3.8%, from 2022. Corn production was forecast at a record-high 15,265 million bushels, with an average yield of 181.5 bushels per acre—both up from 13,895 million bus and 171.9 bus per acre from last year’s forecast.

Somebody is getting taken to the cleaners. But it’s not going to be you.

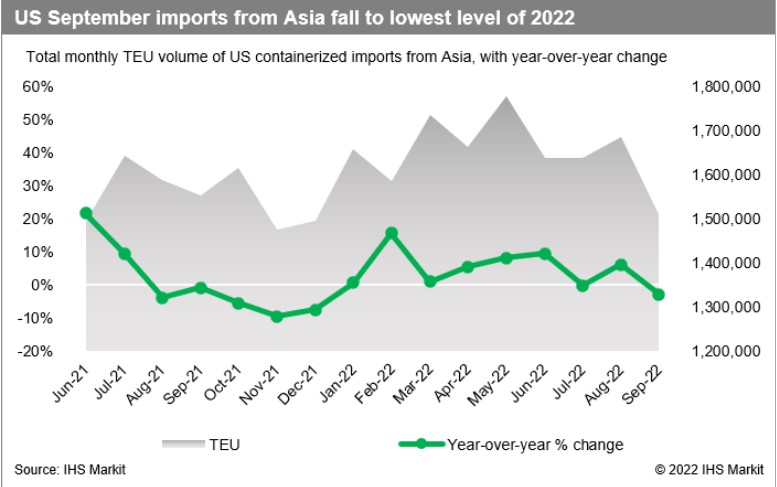

Logistics

After more than two years of record-high freight rates and historic disruption driven by pent-up consumer demand during and in the wake of pandemic-related lockdowns, the ocean transportation market has taken another 180-degree turn. Concern continues to mount as multiple central banks have aggressively raised interest rates to combat inflation. As of late November, spot rates in the eastbound trans-Pacific were creeping below pre-pandemic levels, a dramatic change from just six months ago that few, if anyone, could have predicted—even if an easing of North American imports from Asia was inevitable (9). Carriers are responding by pulling capacity out of the market, while shippers, carriers, and forwarders are assessing what this could mean for the next round of service contract negotiations. As 2022 winds down, industry stakeholders are looking to what’s next, starting with the earlier-than-usual Chinese New Year and the months that will lead up to new service contracts in the spring.

I think—barring any unforeseen calamities—container prices should continue to fall. This is good news, particularly for imported materials coming from China.

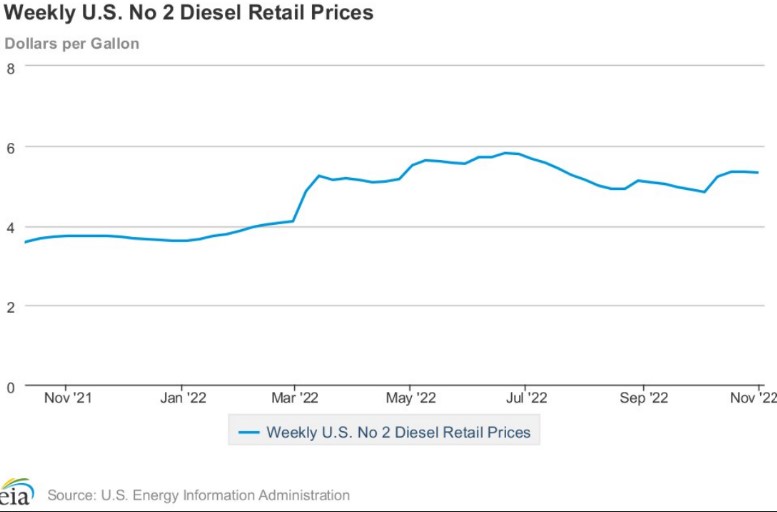

Unfortunately, the price of diesel in the US is still very high. The White House’s promise that America will stop drilling for domestic oil just before the mid-terms might lead to higher fuel costs (3).

While fuel remains a concern, there is good news—the worst of the labor search is over. With an abundance of drivers, labor costs are experiencing downward pressure. Additionally, there were more motor carriers registered and active at the end of September than there were in January 2022 or December last year, according to both the Federal Motor Carrier Safety Administration (FMCSA) and QualifiedCarriers.com (5). More competition means lower prices; less imports means better pricing for manufacturers. Overall, prices will continue to lower as logistics begin to normalize.

Tariffs

This could be a can of worms. If the White House is pressured into implementing anti-dumping tariffs, it could get ugly. I am keeping a close eye on the situation and staying heavy in all raw materials, particularly corn derivatives. A couple of months ago, the Biden administration asked for public comment on the effectiveness of Trump-era tariffs on hundreds of billions of dollars of Chinese merchandise imports as part of its broader review of the duties.

The Office of the US Trade Representative is seeking public comments on “the effectiveness of the actions in achieving the objectives of the investigation, other actions that could be taken,” and the effects on the US economy and consumers (10). The window for comments opened on November 15th and closes January 17th. Make your voice heard. Click here and register your comment.

Erythritol

Icon Foods has boots on the ground in China evaluating our supply chain partners’ positions.

- The new factories that came online when prices were about $8.00 per kilogram have dropped their prices to less than half of what they were previously. This action was taken because of downward pressure on sales. These suppliers are selling their stock at a loss.

- The top three manufactures have dropped their prices by 50% or more FOB China. These top manufacturers are also heavy in material. It seems they are having a hard time turning a profit since the newcomers started selling at a low price.

- According to these manufacturers’ estimates, the cost of energy to drive their production is higher than the price they are commanding for erythritol. This cannot continue for long. Secure your positions now!

- The top three polyol manufactures are holding prices until the start-ups run out of money, eventually run out of stock, and stop producing material. This strategy will drive prices up in Q1.

We are seeing low pricing, cheap logistics, and tariffs. Prices are below 2018 levels. Now is the time to buy. When this cheap stock runs out, prices will likely increase by 25%. By Q2 2023, pricing could return to 2020 levels. Worst case scenario, they’ll be even higher if the situation around corn remains and the conflict in eastern Europe continues. This is where hedging this market makes brilliant sense.

This is vetted data. Not sales hype. Call your Icon Foods representative and let us help you through the potential supply chain storm.

Allulose

There were several new high-quality producers of crystalline allulose that were scaled in 2022. This created strong downward pressure on pricing. Over the last quarter, prices dropped by about 16%. The price remains high on crystalline allulose, despite the over-stocked material available. Meanwhile, the price of allulose syrup remains stable. The conversion from glucose or starch is still not efficient, so pricing could move out of reach with the price of corn in Q2 of 2023. Allulose is one of the best non-nutritive sweeteners, in my opinion. It is easy to use in formulation and plays very well with other sweeteners and fibers. However, it remains pricey. With consumers tightening their belts for the next six months, keeping your COGS low should be a priority. Using monk fruit and or stevia with allulose will save you money and allow you to stretch the allulose further. If you need assistance with conversion, Icon Foods is here to help.

Stevia

Something happened a couple month ago that might put upward pressure on high intensity sweeteners like stevia, monk fruit, and thaumatin. Anhui Jinhe Industrial Co., Ltd. is a China-based company principally engaged in the production and sale of food additives, including the sweeteners acesulfame and sucralose. Last month they had a substantial chemical fire that took out one of their plants (1). There were already shortages for AceK and sucralose (gag.), the destruction of one of their plants will likely exacerbate those shortages and drive-up prices. This opens the door for formulators to move off this chemical stew and onto something clean label.

In Q1 of 2022, there was a significant jump in stevia pricing. This followed a jump in monk fruit pricing. Although these numbers could very well be artificial, since we’ve seen a pullback and stabilization in the past month. The new harvest came in strong the later part of this year and there is reason to believe we will see downward pressure on pricing. Worst-case scenario, we’ll see flat pricing if the demand doesn’t drive up the price.

Monk Fruit

Monk fruit remains the belle of the ball for natural high intensity sweeteners. There was a significant spike in price in Q2 of 2022 followed by stabilization in Q4 of 2022 after a very solid harvest. There continues to be slight downward pressure on pricing, but for the most part it’s stabilized. The fruitful harvest helps keep prices stable. There may be a selloff of 2021 material late Q1 as suppliers try to churn remaining stocks. Prices are stable right now but there will be a buying opportunity in mid to late Q1. Stand by for this.

Xylitol

Xylitol prices have been coming down and are stabilized. We get a lot of questions about why xylitol is so expensive. The answer: water and power. It requires a lot of water and a lot of power to get the d-xylose out of the corn cobs and corn by-products. Expensive electricity and a heavy tax on water usage in China contribute to the price. Most xylitol is derived from corn cobs, which do not birch as some people have been led to believe. Since xylitol is a corn derived ingredient, the price rises and falls in tandem with corn’s price and availability. This would be an ingredient worthy of hedging right now since polyols across the board are at historic lows.

Inulin

Chicory root inulin is back in supply. The supply is good, despite the war in Ukraine. The pricing is also stable—even down some—since a lot of manufactures moved away from chicory root inulin when the price was sky high and supply chains were nonexistent. Jerusalem artichoke and agave inulin are certainly stable, but they’re still somewhat pricey. It appears the abundance of chicory root inulin in the market is putting downward pressure on them. Over the past couple of years, we have moved many of our customers to FOS. While FOS may not have the jelling properties of chicory, Jerusalem artichoke, or agave—mostly because of chain length—FOS still holds up well in most processes and is a fantastic prebiotic fiber. Mixing FOS with soluble tapioca fiber will give you excellent gelling and it stabilizes whatever potential gastro-intestinal issues that may occur from too much dietary fiber.

FOS [Fructooligosaccharides]

Icon Foods is well stocked and well positioned with FOS. The price is very good and can save manufactures money when it comes to inulin. One of the best value propositions of FOS is labeling. It shows up well on the NFP, but also gives you flexibility on the ingredient statement. FOS can be called a prebiotic fiber, FOS, or inulin. When the market eventually shifts, you can interchange FOS and inulin in your formula without having to change all your packaging. Food for thought when considering your fibers.

Soluble Tapioca Fiber

From an Icon Food’s perspective, soluble tapioca fiber is the gold standard for fiber. The price will not be driven up by the corn market. It is not manufactured in China, so it’s not subject to the 25% tariff. Functionally, it is an RS4 resistant dextrose (or resistant starch) that adds fiber and works well in keto and low carb products—as well as applications where fiber is needed to contribute to mouthfeel. Icon Foods is very well positioned in soluble tapioca fiber. The price is much lower than soluble corn fiber and you won’t have to add “corn” in your ingredient deck.

Summarizing Imports Intel

Honestly, I had high hopes for 2022. That is what I get for hoping. There were ups and downs. There has been around a 30% pull back in the keto, low carb, zero sugar added categories—but these are starting to level out. Clean Label Sugar Reduction will always be a thing. But when consumers must decide between a $10 bag of zero sugar added clean label cookies or a $1.29 bag of Chips Ahoy and gas in their car… you see where I’m going with this. There is a lot of encouraging news that inflation has slowed, and consumers are once again looking for healthy options. You will see this in your Q1 and Q2 sales. Count on it.

Thank all of you for your kind comments regarding my last market intelligence report. It means a lot. What would mean even more is if you told me what I can do better and how Icon Foods can be a resource for you.

Thank you for your continued support,

Thom King

CEO & Chief Food Scientist

Sources

- “Anhui Jinhe Industrial Plant Fire Leaves One Dead: Marketscreener.” MarketScreener, 4 Nov. 2022, https://www.marketscreener.com/quote/stock/ANHUI-JINHE-INDUSTRIAL-CO-11367290/news/Anhui-Jinhe-Industrial-Plant-Fire-Leaves-One-Dead-42206649/.

- Barone, Adam. “Dumping.” Investopedia, 8 Feb. 2022, https://www.investopedia.com/terms/d/dumping.asp.

- Blackmon, David. “Biden Promises ‘No More Drilling’ Just Days after Demanding More Drilling.” Forbes, 8 Nov 2022, https://www.forbes.com/sites/davidblackmon/2022/11/07/biden-promises-no-more-drilling-just-days-after-demanding-more-drilling/?sh=52ab418878e7.

- Braun, Karen. “U.S. Corn Market Share Threatened by Importers and Fellow Suppliers Alike.” Hellenic Shipping News Worldwide, 7 Nov. 2022, https://www.hellenicshippingnews.com/u-s-corn-market-share-threatened-by-importers-and-fellow-suppliers-alike/.

- Cassidy, William B. “US Truck Capacity Shifting as Spot Rates Drop.” Journal of Commerce, 4 Nov. 2022, https://www.joc.com/us-truck-capacity-shifting-spot-rates-drop_20221104.html.

- Donley, Arvin. “Global Grains Production Forecast to Decline.” Baking Business, 17 Nov. 2022, https://www.bakingbusiness.com/articles/57834-global-grains-production-forecast-to-decline.

- Ganti, Akhilesh. “Futures Strip Definition.” Investopedia, 8 July 2022, https://www.investopedia.com/terms/f/futuresstrip.asp.

- Hanbury, Shanna. “Bad Weather Knocks down Brazil’s Grain Production as ‘Exhaustively Forewarned’.” Mongabay Environmental News, 17 Aug. 2022, https://news.mongabay.com/2022/08/bad-weather-knocks-down-brazils-grain-production-as-exhaustively-forewarned/.

- Mongelluzzo, Bill. “Falling Spot Rates, Strong Imports Give Rise to Trans-Pac Disconnect.” Journal of Commerce, 29 July 2022, https://www.joc.com/article/falling-spot-rates-strong-imports-give-rise-trans-pac-disconnect_20220729.html.

- Monteiro, Ana. “US Seeks Public Comment on Review of Trump-Era China Tariffs.” Bloomberg, Bloomberg, 12 Oct. 2022, https://www.bloomberg.com/news/articles/2022-10-12/us-seeks-public-comment-on-review-of-trump-era-china-tariffs.